You are now leaving Centuria Australia

and entering Centuria New Zealand.

by Jason Huljich, Joint CEO

As we hit the three-month milestone since Australia went into lockdown, we are starting to get a better gauge of the COVID-19 impacts and emerging market opportunities across the commercial real estate sectors. This historic period provides no roadmap nor compass but, like any new frontier, I believe those who navigate the best course of action now, will claim the biggest stakes. On a global scale, it seems Australia is on the right road to recovery.

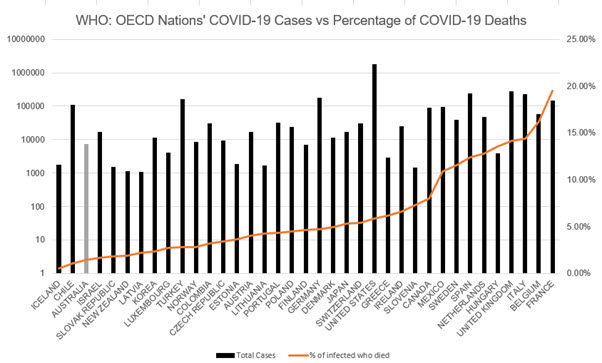

First, there is a lot to be said about ‘early mover advantage.’ Australia was one of the first nations to close its borders and send its workforce home. We currently have an extremely low number of COVID-19 infections and experienced a limited number of COVID-deaths, especially in comparison to other OECD Nations. Australia has the third lowest death rate[1] among the 37 countries, as illustrated in the graph below.

Arguably, this could mean Australia is poised to be among the first economies, to get back to work, restart productivity and kick-start commerce.

Source: WHO Coronavirus disease (COVID-19) Situation Report – 135. Data received by 10:00 CEST, 3 June 2020

Australia’s GDP for the March 2020 quarter outperformed many other nations. Australia’s GDP fell by only 0.3%, while the US was down 1.3%, Canada down 2.1%, Japan down 0.9%, Britain down 2.0% and Germany down 2.2%[2]. It is quite likely that the current June quarter, the period the world went into lockdown, will show further decline in GDP, resulting in a technical recession. However, Australia is most likely to experience a shallow recession rather than a more significant decline, like that experienced in the 1991 recession. The OECD has predicted the local economy could rebound 4.1% by 2021 if a “second-wave” of COVID-19 is avoided. I also believe that growth will be achieved in the third quarter of the calendar year.

Arguably, Australia also found the right balance between border and business closures while continuing commerce and trade with employees working from home. Across the Tasman, New Zealand implemented much stricter restrictions and ANZ New Zealand chief economist Sharon Zollner predicts the country’s GDP would be eight to 10 per cent lower this Christmas compared to last year[3]. It’s interesting to note Australia’s cash rate is also better than New Zealand’s.

Complementing the relative health of the nation is the healthy federal Government’s $214 billion economic support package, which includes the largest bond sale in Australian history. Recently issued 10.5-year bonds have injected $19 billion into domestic economy. This means more liquidity.

Government intervention in the commercial property sector, extends to the Federal Government Code of Conduct, which prioritises Small to Medium Enterprise (SMEs) tenants and prioritises tenants precluded from trading. The latter referring to tenants who have a turnover of less than $50m, experienced greater than 30% decline in turnover; and are eligible for the JobKeeper subsidy.

This is to act as a safety net for smaller operators.

Fund Managers with property portfolios occupied by Multinational Corporations (MNCs), listed entities and Government departments are less likely to be affected by rental arrears as well as rent relief offered under the Code. This has a knock-on effect for returns and distributions. These larger entities also tend to be more resilient in their operation and can continue to contribute to the economy.

However, the protection of vulnerable tenants means business can more quickly return to trading when restrictions lift, and society can function as normal. Without smaller operators, there would be a hole for the missing functions these operators provide in the economy.

Additionally, the Reserve Bank of Australia (RBA) has held cash rates at 0.25% since 20 March 2020, the day restrictions and social distancing were implemented. These historically low rates have never been experienced in Australia, and they look likely to hold in the medium-term. This enables competitive swap rates, resulting in cheaper debt that enables businesses to increase headroom on their balance sheets. For businesses in distress, it’s a sigh of relief as they are better able to make repayments.

Low interest rates also generate a strong appetite for real estate as investors search for attractive yields. This is true for both onshore and offshore investors. In comparison to other investment classes that are reliant on robust interest rates, such as bonds, income investments, and term deposits, direct property investment and REITs, have become more appealing.

From a household perspective, the low interest rates complement the newly announced $688m HomeBuilder stimulus package, which provides those eligible with a $25,000 cash grant for new housing and home renovations. From a fiscal perspective, it supports skilled-based jobs, such as carpentry, electrical and plumbing, for the coming six months. Again, great initiatives to support the economy.

From a commercial real estate perspective, lower debt levels also spur opportunities for growth and expansion by acquisition. Unlike other downturns, when distressed assets created opportune buys, the volume of assets for sale may be limited. This is because, previously, “distress” resulted from a Landlord’s inability to meet loan repayments but with currently low interest rates, owners with quality tenants are more likely to be able to meet debt obligations.

Despite fewer assets on the market, there are still acquisition opportunities as operators realign their business strategies. Sale and leaseback options have been popular across the industrial and logistics markets throughout the past several months. The lockdown has also prompted more online shopping, adding to the demand for logistics and distribution centres from traditional and non-traditional retailers and grocers.

Workers are also starting to return to their offices. Distancing requirements means lettable space is unlikely to shrink despite fewer workers in the office. I believe this is a short-term change in workforce requirements and unlikely to have a material impact on demand for the medium to long-term.

Balance sheet capacity and lower debt costs also prompts M&A activity as companies look to grow. Recently, Centuria secured a 23% stake in a New Zealand peer, Augusta Capital. The size of the New Zealand commercial real estate market is comparable to some Australian capital city markets, providing good investment opportunities.

As I mentioned earlier, there’s no precedent to determine the road – socially and economically – to Australia’s COVID-19 recovery. However, I believe Australian commerce is on good footing and we are ahead of the curve in comparison to international markets. On the commercial real estate front, this puts our sector in the limelight from both a domestic and international perspective.

[1] Calculated by the number of COVID-19 cases compared to the number of those who died from COVID-19, as a percentage.

[2] SBS World News Australia

[3] https://www.smh.com.au/world/oceania/first-coronavirus-now-the-nz-economy-ardern-s-next-challenge-20200609-p550yn.html